The 3% Interest Rate "Golden Cage": How to Finally Sell Your Columbus Home and Move Up (Without Regretting It)

The 3% Interest Rate "Golden Cage": How to Finally Sell Your Columbus Home and Move Up (Without Regretting It)

Have you ever felt completely trapped by something that’s supposed to be a good thing?

It’s like owning a gorgeous pair of designer shoes that are two sizes too small. They look absolutely amazing sitting on your closet shelf, but the second you put them on and try to walk down Broadway in Grove City, your feet are begging for mercy.

That is exactly how a lot of Central Ohio homeowners are feeling right now about their mortgage rates.

If you bought or refinanced a home around 2020 or 2021, you’re likely sitting on an ultra-low interest rate of 2.75% or 3%. On paper, it’s a financial dream. But in reality? Your family has grown, you’re drowning in toys, you desperately need a quiet home office, and your current house is practically bursting at the seams.

Welcome to the "Golden Cage." It’s the psychological trap of holding onto a home that no longer fits your life, simply because you don't want to trade a 3% rate for a current rate in the low-6% range. But here is the unfiltered truth: you cannot live in an interest rate. If you are ready to break free and find a home that actually matches your lifestyle, here is how to mathematically and emotionally make the move in today's market without an ounce of regret.

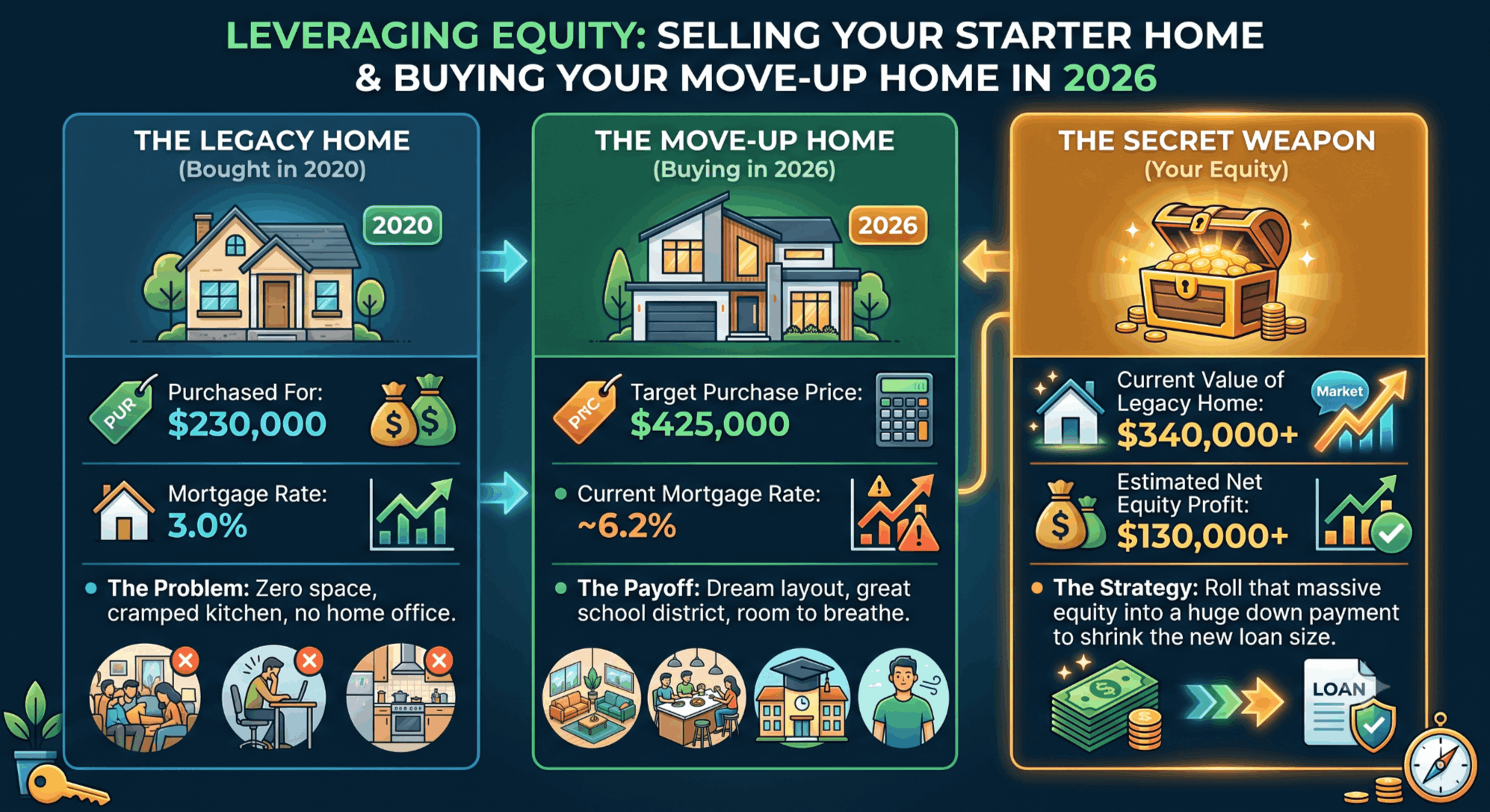

The Reality Check: 2020 vs. 2026

To understand how to make this move successfully, we have to look at the whole financial picture. Here is what the math actually looks like for a typical Columbus homeowner making a move today:

1. Unleash Your Secret Weapon: Columbus Home Equity

If you’ve been living in your house for the last four to six years, you are sitting on a mountain of cash. Thanks to the massive Silicon Heartland tech expansion and steady demand across Greater Columbus, local property values have climbed significantly.

When you sell your current home, you aren't just walking away with a few thousand bucks—you are likely walking away with a massive, six-figure check.

By rolling that equity directly into your next home, you radically reduce the amount of money you actually need to borrow. A smaller loan balance means your monthly payment at a 6% rate might be shockingly close to what a larger loan would have been at 4%.

2. Think in "Blended Rates"

If you still feel uneasy about today's rates, look at it through the lens of a blended rate.

Let’s say you have some credit card debt, a student loan, or a car payment with an 8% to 15% interest rate. If you use a portion of your home equity to completely wipe out those high-interest monthly debts, and then take on a 6.2% mortgage on a bigger house, your overall household interest rate profile actually drops.

You are lowering your total monthly layout of bills, even though your housing note went up. Suddenly, the move feels a lot more comfortable.

3. Don’t Let the "Wait and See" Game Cost You More

We talk to so many homeowners who say, "Adam, I'm just going to wait until rates drop back to 4.5% before I list my house." It sounds like a safe bet, but it’s actually a high-risk gamble. Remember: you are not the only person with this plan. The exact second mortgage rates drop significantly, a tidal wave of frustrated buyers is going to flood the Central Ohio market.

What happens when demand explodes and inventory can't keep up? Severe bidding wars return, and home prices will skyrocket. You might save a percentage point on your interest rate, but you’ll end up paying $40,000 more for the exact same house.

By making your move now while the market is balanced and predictable, you can negotiate calmly, keep your inspection contingencies, and buy at a fair price. If rates drop later? You can always refinance.

4. Prioritize Your Quality of Life

At the end of the day, real estate isn't just an entry on a financial spreadsheet—it's where your life happens.

No one lies awake at night dreaming about an interest rate. They lie awake dreaming about having a backyard where the kids can run around, a kitchen island big enough for Sunday morning pancakes, or a quiet space to work from home without a dog barking in their ear.

If your current house is actively causing you daily stress, that 3% interest rate isn't saving you money; it's costing you peace of mind.

Let’s Crunch the Real Numbers Together

Breaking out of the "Golden Cage" doesn't mean making a reckless financial leap. It means getting an honest, clear-eyed look at what your house is worth today and mapping out a smart, strategic transition to your next chapter.

Curious to know what your Central Ohio home is worth in today's market? Drop us a line at Hagenstein Real Estate. We will put together a zero-pressure, highly accurate home valuation and show you exactly how much equity you have to work with. Let’s get you into a home you actually fit in!

Categories

Recent Posts

REALTOR® | Investment Specialist | License ID: 2020002093

+1(614) 505-4510 | ahagenstein@hsrellc.com