Demystifying the Mortgage Process

The First Step to Your New Front Door: Demystifying the Mortgage Process

Let's be honest: the most fun part of buying a house is the house hunting. Spending your evenings scrolling through listing photos and imagining where your furniture will go is exciting! But as a real estate professional with over 20 years of experience, I’m going to let you in on a little industry secret.

The real first step to buying a home doesn't happen on a property tour. It happens at a lender's desk.

At Realty Forward and HSRE LLC Real Estate Solutions, I always tell my clients that understanding the lending process is the true foundation of a successful home purchase. It can feel like a maze of paperwork and financial jargon, but it doesn't have to be overwhelming. Let’s break down the home lending process together so you can shop with absolute confidence.

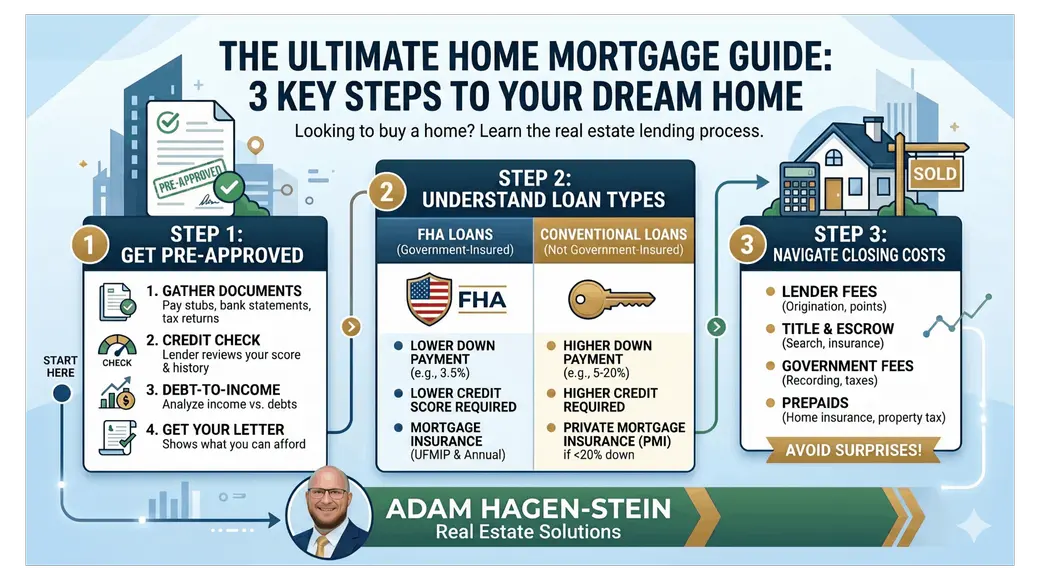

The Golden Ticket: Why Pre-Approval Comes First

Before we step foot inside a single open house, we need to get you pre-approved for a mortgage. Why? Because looking at homes without a pre-approval is a bit like grocery shopping without your wallet.

Getting pre-approved does two crucial things:

-

It protects your heart. There is nothing worse than falling in love with a property only to find out it's outside of your financing reach.

-

It makes your offer strong. In a competitive market, a seller won't even look at an offer if it doesn't have a pre-approval letter attached. It proves to the seller that you are a serious, qualified buyer who can cross the finish line.

The "Holy Trinity" of Lending: Credit, Income, and Job History

When you apply for a pre-approval, the lender is essentially trying to answer one question: Is this person a safe bet to lend money to? To figure that out, they look at three main areas:

-

Good Credit: Your credit score is the key that unlocks the best interest rates. A strong history of paying your bills on time shows lenders you are responsible with debt.

-

Great Income: Lenders will calculate your "debt-to-income ratio" (DTI). They want to make sure you make enough money to cover your existing debts plus a new mortgage.

-

Solid Job History: Lenders love stability. Typically, they want to see a consistent, two-year history in the same job or at least the same industry.

To prove all of this, your lender will ask for a mountain of documents. Be prepared to hand over recent pay stubs, the last two years of W-2s and tax returns, and recent bank statements. Gathering these early will save you a lot of stress later!

Your "Comfort Zone" vs. Your Approval Amount

Here is a piece of advice I give to every single client: Just because a lender approves you for a certain amount doesn't mean you have to spend it.

Lenders approve you based on maximum thresholds, but they don't know how much you like to spend on groceries, travel, or daycare. Instead of focusing on the highest purchase price you can get approved for, focus on your comfortable monthly payment.

When you buy a home, your monthly payment isn't just the loan. It's an acronym we call PITI:

-

Principal (paying down the actual loan balance)

-

Interest (the cost of borrowing the money)

-

Taxes (property taxes)

-

Insurance (homeowner's insurance)

Always work backward. Figure out the total monthly payment that lets you sleep peacefully at night, and we will find a beautiful home that fits that exact budget.

Mortgage Alphabet Soup: Types of Loans

There is no "one size fits all" mortgage. Depending on your financial profile, your lender might recommend one of several different types of mortgages:

-

Conventional Loans: The most common type of loan. These are great if you have a strong credit score and a solid down payment.

-

FHA Loans: Backed by the Federal Housing Administration, these are incredibly popular for first-time homebuyers because they offer more flexibility with credit scores and require a lower down payment.

-

VA Loans: Reserved for our active-duty military and veterans (thank you for your service!). These amazing loans often require zero down payment and have highly competitive interest rates.

-

USDA Loans: Designed to encourage homeownership in rural and some suburban areas. These also offer zero-down options, though they come with specific geographic and income limits.

The Cash Needed to Close

Finally, let's talk about the cash you'll need to bring to the table. Buying a home requires two main buckets of funds:

1. The Down Payment Let's bust a major myth right now: You do not necessarily need 20% down to buy a house. While putting 20% down helps you avoid Private Mortgage Insurance (PMI), many loan programs allow for much lower down payments—sometimes as low as 3% or 3.5% for qualified buyers.

2. Closing Costs These are the administrative fees required to process your loan and transfer the property. They include things like the home appraisal, title search, lender origination fees, and setting up your escrow account for taxes and insurance. Closing costs generally equal a small percentage of your total loan amount. While I can't give you a specific dollar amount until we look at a specific house and loan, your lender will provide you with a "Loan Estimate" upfront so you know exactly what to expect. No surprises!

Let's Navigate This Together

The lending process is a journey, but you don't have to walk it alone. Having a great real estate agent in your corner means having a guide to help translate the paperwork, connect you with trusted local lenders, and advocate for your best interests.

If you are ready to start the exciting journey toward homeownership, reach out to me today. Let's get your financing dialed in so we can go find your perfect home!

Categories

Recent Posts

REALTOR® | Investment Specialist | License ID: 2020002093

+1(614) 505-4510 | ahagenstein@hsrellc.com